How KLIMA inverse bonds will impact the ReFi ecosystem

KlimaDAO has increasingly mentioned something called "inverse bonds". What are they, when will they be triggered, and which consequences might arise?

Background

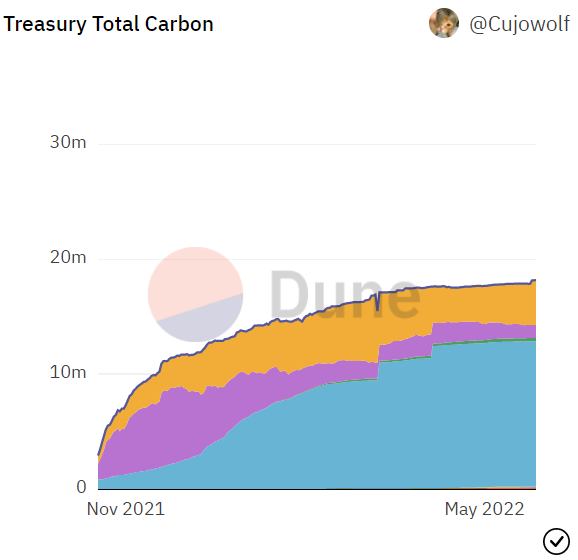

The by far largest holder of tokenized carbon credits is Klima DAO, with over 18 million tonnes safely locked away in their treasury: the so called “black hole” for carbon.

However, those following the Klima DAO community closely, may have noticed an increased mentioning of something called inverse bonds. In this article, we will explain what inverse bonds are, when they will be triggered and explore the impact of inverse bonds on BCT and the on-chain carbon markets.

What are inverse bonds?

Klima is a carbon-backed currency, with a set of complicated mechanisms. But simply put, it works as follows: Market participants can sell their carbon credits at a discount to Klima in exchange for newly minted Klima-tokens (this process is referred to as bonding). Participants that hold Klima can “stake” their Klima, which locks it up in exchange for receiving a portion of newly minted Klima tokens (practically this works very similar to a stock split). Through these mechanisms, the supply of Klima inflates whilst an increasing amount of carbon is bought and stored in the treasury.

Now inverse bonds are more or less the same bonding process as described above, but inverse. Klima DAO describes inverse bonds as follows

In the event that KLIMA were to trade persistently below IV (Intrinsic Value), as a last resort the policy team plans to launch inverse bonds, which accept KLIMA in return for BCT at a discounted rate, and then the bonded KLIMA is burned, shrinking the supply of KLIMA.

This mechanism exists to protect the value of Klima, to ensure if the token is trading far below what it is worth, the protocol can back it up. This is done by selling treasury assets in exchange for Klima. In February 2022 a proposal to allow the Policy Team to enact inverse bonds was approved in governance.

It is important to note the following about inverse bonds:

- Inverse bonds will only be enabled when the price of 1 Klima goes below 1 BCT

- There have been repeated commitments to protect the 1 Klima = 1 BCT peg through inverse bonds

- The Klima team are working to prepare and test inverse bonds

At the time of this writing, Klima trades at 4.96$ and BCT trades at 2.12$, however, 30 days ago Klima traded at 16.9$. The gap between the price of BCT and Klima is rapidly closing, as the supply of Klima inflates and generally poor market conditions push down the price far below its treasury value. It is difficult to predict how the price of Klima and BCT will evolve in the next weeks and months, but the risk of 1 Klima trading at or below 1 BCT is growing.

We have for several months been monitoring and modelling this relationship, but it has always seemed to be a distant risk. Because of the increased likelihood of this happening, we would like to share our analysis, to help our respective communities understand the possible impacts on the carbon markets, and take well informed decisions. To be clear, no-one can fully predict what will happen with Klima inverse bonds as this has never been done before, but we have done our best to model its impact based on scenarios informed by Olympus inverse bonds.

The impact of inverse bonds

In the same way bonds cause buying pressure on bonded assets, inverse bonding cause selling pressure. The path to leverage inverse bonds will be different for different actors, but in general, it would look something like this:

- Trade USDC for Klima

- Inverse bond Klima to receive BCT

- Sell BCT to receive USDC

In this example, there is increased buying pressure on Klima and selling pressure on BCT. This should increase the price of Klima and decrease the price of BCT.

In an example of USDC inverse bonds, it would look something like this:

- Trade USDC for Klima

- Inverse bond Klima for USDC

Alternatively:

- User holds Klima and wants to exit their position

- Inverse bond the Klima for USDC

A key question is: What assets will be inverse bonded?

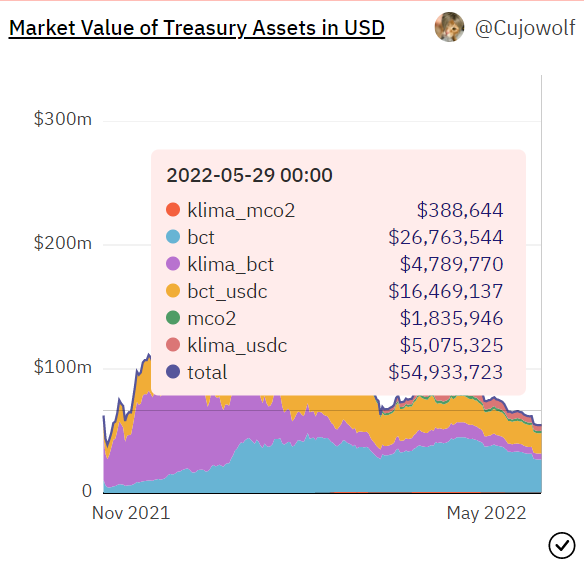

From the Klima DAO dashboard (at the time of this writing), it is clear the vast majority of value in the treasury is BCT and BCT liquidity (about 48m$ or 87%). The DAO wallet furthermore has 4.3m$ of USDC which is not included above. This graph also doesn’t factor ownership of NCT, NBO, UBO, though these are marginal. There are four paths Klima could take to inverse bonding:

- Inverse bond USDC from the treasury

- Inverse bond an even share of all tradable assets

- Inverse bond BCT because it is the most liquid treasury asset

- Inverse bond anything other than BCT to avoid crashing the treasury

The following scenarios were calculated using the current liquidity (29.5.2022) and price impact of executing this as a single trade, assuming no slippage or fees, which obviously is a significant simplification of reality. Inverse bonds gradually release these assets, so the actual impact would be spread out over many trades and a period of time. This would ensure the slippage from each trade would be relatively small. If you argue there is more demand for the assets at lower prices, the impact may be dampened. If you believe traders will front-run inverse bonding operations the impact may be exacerbated. It is impossible to precisely model the impact of inverse bonds, as one cannot predict the actions of other market participants. However, despite the limitations of this methodology, we can still explore the directional impact of various policy choices.

Impact of inverse bonding USDC

Klima DAO intends to primarily enable USDC inverse bonds, which means Klima holders can exchange their Klima for USDC. This has a few significant benefits:

- No treasury assets receive selling pressure

- Inverse bonding of USDC will increase the price of Klima and therefore the bond capacity, which may create positive buying pressure on other treasury assets

- Market participants who may want to exit their Klima position would get the option to inverse bond their Klima for USDC, instead of selling it on the market, which will reduce selling pressure

With current available USDC (which would need to be unlocked through a KIP - Klima Improvement Proposal), there could be a 43% increase in Klima price from buying pressure resulting from bonding 4.3m$ USDC. Furthermore, Klima DAO holds about 8m$ USDC in its BCT-USDC LP position, which with another KIP could be accessed to further inverse bond Klima. It is likely it would take a significant amount of time to inverse bond the combined 12.3m$ of USDC that Klima DAO has at its disposal. And it seems highly unlikely that Klima DAO would start inverse bonding any other treasury assets before depleting most of its USDC reserves.

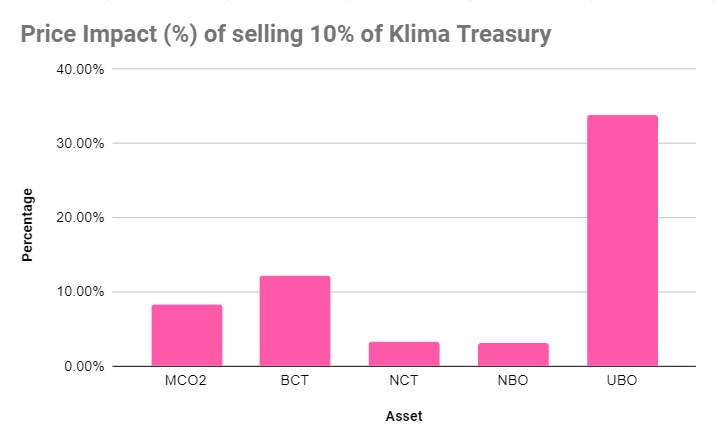

Impact of selling 10% of all non-liquidity treasury assets

In the second scenario, where an even distribution of treasury assets is sold (excluding the USDC), there will be a wide-spread impact on all major carbon tokens on-chain. The size of the impact will depend on the amount of assets sold, but using a hypothetical scenario of 10%, there is a varying impact across the space, depending on the relation between assets owned by Klima DAO and those assets’ liquidity.

In the above example, there would be quite a significant impact on UBO, a moderate downward pressure on MCO2 and BCT, whilst only a marginal impact on NCT and NBO. A total of 2.9m$ of carbon would be released in exchange for Klima tokens, that at current Klima liquidity levels could create a 29% increase in Klima price. An increased price of Klima would increase bond capacity, which could have a positive impact on bonded assets over time, if the price of Klima remains elevated. Meanwhile, the loss of carbon in the treasury, as well as reduced price of such carbon (including in Liquidity Provier - LP positions), would produce a loss in treasury value of 8.29m$ or 15% of all treasury value. So whilst there is potential to increase the price and asset backing per Klima-token, it would be at a significant cost to its treasury which itself may be negative for the value of Klima.

This highlights the fundamental issue with inverse bonding carbon for Klima DAO. Because there is limited demand for on-chain carbon, the prices of these assets are in the short term driven by selling and buying pressure, and Klima DAO is by far the biggest holder of this carbon, including its liquidity. This means the actor that by far loses the most from inverse bonding these assets is Klima DAO. This is why the policy team are going to prioritize using USDC for inverse bonding, and it is likely that inverse bonding other carbon assets will only be a last resort if all USDC is depleted. This means the community will likely have quite a long heads-up before there is any impact on carbon assets, even if USDC inverse bonds were implemented in the short term.

Impact of selling only BCT

In the scenario of only selling BCT, we have assumed 20% of BCT is inverse bonded. This amount of BCT inverse bonded would reduce its price by 24.5%. The impact on the treasury would be a reduction in value of 13.1m$ or 23.9%. However, this would produce 5.3m$ of buying pressure on Klima, which could raise its price by 53.5%. As the above example shows, there would be a significant loss in treasury value by inverse bonding such a large amount of BCT. There is a case to only inverse bond BCT, because it is the most liquid asset in the treasury (after USDC), but given the relatively high concentration of treasury value in this asset, there is also a strong case to be made to not inverse bond BCT.

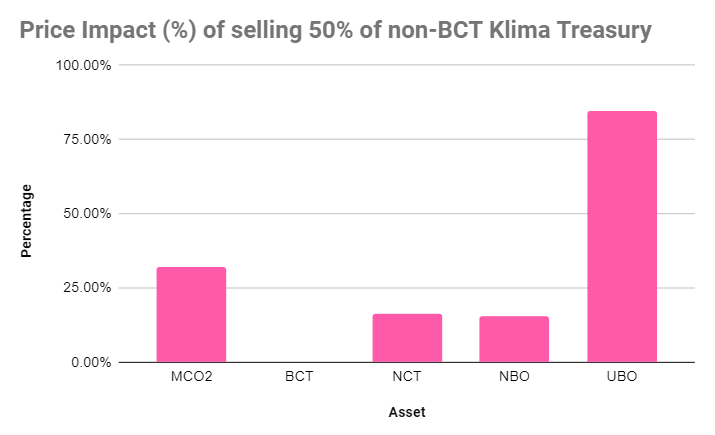

Inverse bonding anything but BCT

In this scenario, to protect the treasury from downward pressure on BCT, all other treasury assets are sold, except BCT, with 50% of such assets being sold in total.

As can be seen in the above graph, there would be a significant impact on the price of multiple carbon tokens, with UBO going dangerously close to 0 and MCO2 dropping to 4.3$. This would meanwhile produce 1.28m$ in buying pressure on Klima, which would increase its price by 12.9%. The treasury would lose about 1.8m$ or 3.35% of the treasury.

What is clear is that selling any asset other than BCT creates a lower loss in treasury value, compared to its impact on buying Klima. However, these assets have thinner liquidity and there is less of them in the treasury so only a limited amount of Klima could be bought. After USDC inverse bonds, there is a case for inverse bonding these assets first, which would be most effective from the perspective of preserving treasury value, but would also reduce treasury diversification and create the biggest % impact on on-chain carbon markets.

In the same way bonding grew the treasury, inverse bonding will shrink it, and likely with it the possible market capitalization of Klima. Inverse bonding USDC is clearly the most favorable option, which could have an overall positive impact on the ecosystem, however, it is clearly not a good idea to inverse bond other treasury assets. The policy team is well aware of this and are very likely to navigate inverse bonds with care.

Impact on so-called “black-hole” narrative

Perhaps the biggest impact of inverse bonding any asset other than USDC, is that it would permanently end the “Klima is a black-hole for carbon” narrative, that assets bonded into Klima DAO, will forever stay there. Klima DAO has over time moved towards a narrative of creating an economy for carbon markets, but given how central the black-hole narrative was for the initial thesis of Klima, and that many in the community joined the mission for this reason, it would be a significant shift if carbon inverse bonds were issued. If Klima DAO will sell carbon from its treasury when it is most profitable for their token price, they are only a temporary holder and trader of carbon, not a permanent carbon sink. Claims of making a positive impact from being a carbon sink would be highly questionable. Holding ownership in a carbon market maker is not comparable to holding ownership in a vehicle that exists to permanently retire carbon. To be clear, carbon inverse bonds have not been issued yet, and perhaps the above narrative challenge may be a reason why they never should.

Toucan has never endorsed using staked Klima for offsetting, and has consistently been advocating for a focus on actual credit retirement, especially of high quality carbon assets, to create climate positive action. We write this not as a way to take away from the work Klima DAO has done to further the regenerative finance community, including encouraging retirements such as through the love letter campaign, which has generated over 150k tonnes of retirements. However, it is important to highlight the importance of making actual retirements. Holding or trading carbon is not equivalent to retiring carbon.

Conclusion

Toucan’s carbon pools are permissionless products that anyone can build with. BCT was designed by Klima DAO for Klima, and since then they have built an ecosystem around this asset. Toucan does not control who buys and sells BCT or NCT. Inverse bonds, if implemented starting with USDC, would likely have a positive impact on on-chain carbon prices, and a positive impact on the price of Klima. However, inverse bonding anything other than USDC, would likely have a negative impact on carbon markets whilst possibly having a positive impact on Klima. The larger impact of inverse bonding assets outside of USDC will be the death of the black-hole narrative, by converting the protocol from a carbon sink to a carbon trader and market maker. Regardless of the path the Klima policy team takes with inverse bonds, we will continue building a diverse ecosystem of use cases with on-chain carbon, and in the absolute worst case the biggest impact of inverse bonds on this ecosystem will be a temporary price decrease, something we likely are all a bit too familiar with in our own portfolios these days.

Big thank you to Marcus, Sy and Brian for their feedback on this article.

Further Resources

- Klima Dashboard

- Klima Docs: Inverse Bonding

- KIP 12: Inverse Bonds

- Klima reaffirm inverse bonding at 1 Klima = 1 BCT

Toucan is building the technology to bring the world's supply of carbon credits onto energy-efficient blockchains and turn them into tokens that anyone can use. This paves the way for a more efficient and scalable global carbon market.